Economic Action Plan, pt. 1

What does the feel-good ad about taxes tell us?

If you still watch television, then you have probably seen the ad. A teenage girl kicks the soccer ball into the top corner of the net as a voice-over reminds you of the all tax savings available from your friendly Canada Revenue Agency.

The ad highlights four separate tax credits: youth fitness, trade tools, public transit and first-home buyers. It then shows an elderly couple skating through life thanks to pension-income splitting and concludes with the now familiar logo of the Economic Action Plan.

Extending income splitting to those still in the workforce is the most expensive electoral promise that Stephen Harper has made in the current campaign.

Only one of these five measures actually has anything to do with Jim Flaherty’s Economic Action Plan: the $750 credit for first-home buyers. The other measures date from the Harper government’s first mandate, from 2005 to 2008.

All of these measures, however, share a common logic. Flaherty’s policies during the boom years shaped the Harper government’s response to the crisis. So, in this the first of a four part examination of what the Economic Action Plan really means, I start with an analysis of what the government has chosen to highlight.

What are these tax credits?

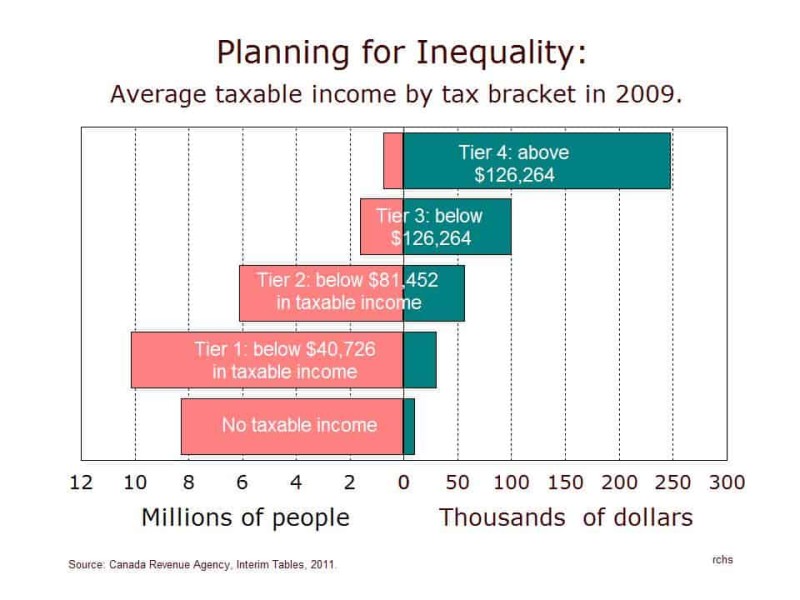

Tax credits are applied against the taxes you owe to the government. They generate refunds only if you have a taxable income. A third of the 24.5 million Canadians, who filed a tax return in 2009, had no taxable income and so they were not eligible for any of these credits.

The credits for fitness and tools are both capped at $75, or 15 per cent of the eligible $500 in expenses. In St. John’s, a soccer-playing teenager would generate a whopping tax credit of $16.50, (15 per cent of the $110 registration fee) enough to pay the HST on his or her cleats.

In 2009, fewer than one in ten Canadians who paid income tax claimed the fitness credit. Revealingly, three-quarters of them were among the one-third in the higher tax brackets. Golf, tennis, horse-riding and hockey are all much more expensive than soccer, but as girls’ soccer is the largest organized sport in Canada, it was chosen as the poster child.

In 2009, fewer than one in ten Canadians who paid income tax claimed the fitness credit.

Tools for the trades are expensive. The ad shows a contented tradesman looking at a very impressive table saw; his $75 credit would not have gone very far. This limited credit for the tools of working people contrasts sharply with the 100 per cent tax write-off introduced by Flaherty for purchases of computers and software by professionals and business people.

Surprisingly, in 2009, most of the public transit credit (53 per cent) also went to people in the higher tax brackets. Monthly and yearly passes on the Go Trains of suburban Toronto are eligible for this credit; the 10-ride pass from MetroBus is not.

Capped at $750, the first-home buyer’s credit would cover only a small part of the cost of buying a home. Not surprisingly, in the midst of the worst economic crisis in more than a generation, two-thirds of those making this claim were in the higher tax brackets.

What is pension-income splitting?

This is the most expensive of the measures. It cost the federal government a billion dollars in 2009, while the provincial and territorial governments, with the exception of Quebec, lost hundreds of millions dollars in revenues. All of the people benefiting from this deduction are in the higher tax brackets, as the only reason to split your pension income is to lower your tax bracket.

This remarkable largesse is not only socially selective, but it has a highly regressive gender component as well. It rewards only those households where there is a significant discrepancy in spousal income. Generally, it allows a husband who has been earning a high income for many years to reduce his taxes in retirement without ensuring that his wife receives any of the benefits. Extending income splitting to those still in the workforce is the most expensive electoral promise that Stephen Harper has made in the current campaign.

What are they not talking about?

The socially skewed nature of each of these diverse measures share a common assumption: lowering taxes on the wealthy benefits everybody, because allegedly “a rising tide raises all boats.” Yet, from Reykjavik, to Athens, on to Dublin and Lisbon, all their boats now lie wrecked in the harbour.

Why has this not been the case in Canada? After all, the same philosophy inspired the Economic Action Plan. The answer is something that both Flaherty and the Harper government have deliberately chosen not to highlight. It is called the Extraordinary Financial Framework. This decision to downplay the largest Canadian government programme since the Second World War is itself highly revealing.

Part two of this series will explore why.

Related Articles

Enabling dependency

How can we explain the continued government inaction in the face of the worst recession since the cod moratorium?

Estimating the damage

What is actually being cut in this budget?

Is there a democratic alternative to austerity?

Other places have experimented with austerity, so we don’t have to. Here’s how Newfoundland and Labrador can avoid known mistakes and put itself on a path to a brighter, more equitable, future.